Donate. If you don't need the money and all your and your family members needs are met, I think donating would be the right ethical thing to do.

this post was submitted on 10 Jan 2025

36 points (92.9% liked)

Ask Lemmy

27401 readers

1262 users here now

A Fediverse community for open-ended, thought provoking questions

Rules: (interactive)

1) Be nice and; have fun

Doxxing, trolling, sealioning, racism, and toxicity are not welcomed in AskLemmy. Remember what your mother said: if you can't say something nice, don't say anything at all. In addition, the site-wide Lemmy.world terms of service also apply here. Please familiarize yourself with them

2) All posts must end with a '?'

This is sort of like Jeopardy. Please phrase all post titles in the form of a proper question ending with ?

3) No spam

Please do not flood the community with nonsense. Actual suspected spammers will be banned on site. No astroturfing.

4) NSFW is okay, within reason

Just remember to tag posts with either a content warning or a [NSFW] tag. Overtly sexual posts are not allowed, please direct them to either !asklemmyafterdark@lemmy.world or !asklemmynsfw@lemmynsfw.com.

NSFW comments should be restricted to posts tagged [NSFW].

5) This is not a support community.

It is not a place for 'how do I?', type questions.

If you have any questions regarding the site itself or would like to report a community, please direct them to Lemmy.world Support or email info@lemmy.world. For other questions check our partnered communities list, or use the search function.

6) No US Politics.

Please don't post about current US Politics. If you need to do this, try !politicaldiscussion@lemmy.world or !askusa@discuss.online

Reminder: The terms of service apply here too.

Partnered Communities:

Logo design credit goes to: tubbadu

founded 2 years ago

MODERATORS

I work in the finance sector, I am IT guy with zero knowledge or interest in investing.

Working in the finance industry binds me to additional rules, I can't buy and sell stocks as I want to, I need pre-approval from the CEO of my company to sell stock for profit (I can still sell at a loss without pre-approval), I need to report any stocks I have to the company as well as any transactions.

So I just don't bother.

I have got a few bonuses, and what I usually end up doing it just putting them in my savings account.

If I did bother I would invest in funds, as they are often less volatile than stocks.

Since it sounds like you have younger kids, I'd take a decent sized portion of it (maybe 2-8k) and use that to make lasting family memories. Seeing everything of interest in a short range (zoos, aquariums, caves, gardens, museums, national parks, whatever), more frequent small vacations (driving distance or short flights to the beach/mountains/whatever), occasional major vacations (other countries, theme parks, cruises, whatever your family finds interesting). Or investing in lifelong hobbies that you can do together, like skiing, art, tennis, restoring cars, etc.

After that, the rest I would add to my FIRE plan. It would not necessarily mean retiring sooner (though it might), but it would be about adding flexibility to my life. If my savings were larger, I could always just to dip into that to pay for college or I be better prepared to deal with an unexpected layoff or emergency.

Similar boat recently, talked to an FA and am now investing. Also got a life insurance policy and LTD policy just in case...

6 months of all of your expenses in a high yield savings is number one. Good times are great, take it from me though, tomorrow they can stop and you'll be back to zero income, when that happens you'll be happy you have that savings.

After that, investing. Very easy to get into, if you don't want to get in right now you can just put the money in CDs and then swap it over to the market later. Not individual stocks, I'm talking index funds and ETFs, things that track the overall market, not a specific company. Then just set it and forget it. Don't check it daily or weekly, just let it sit and make you more money.

Treat investing as just another expense, that has the lowest priority. As Warren Buffet says, pay yourself first. So first pay your bills, then your savings, then with what ever is left as the other commenters said, set aside X amount for fun play money (and it's good to have a number for this, that number can spiral if you don't control it, all of a sudden you just spent 2 grand on a GPU you didn't need), and then put in your Y amount into investing. When times are good it is good to set everything you can for the future. You'll be happy when times aren't so good.

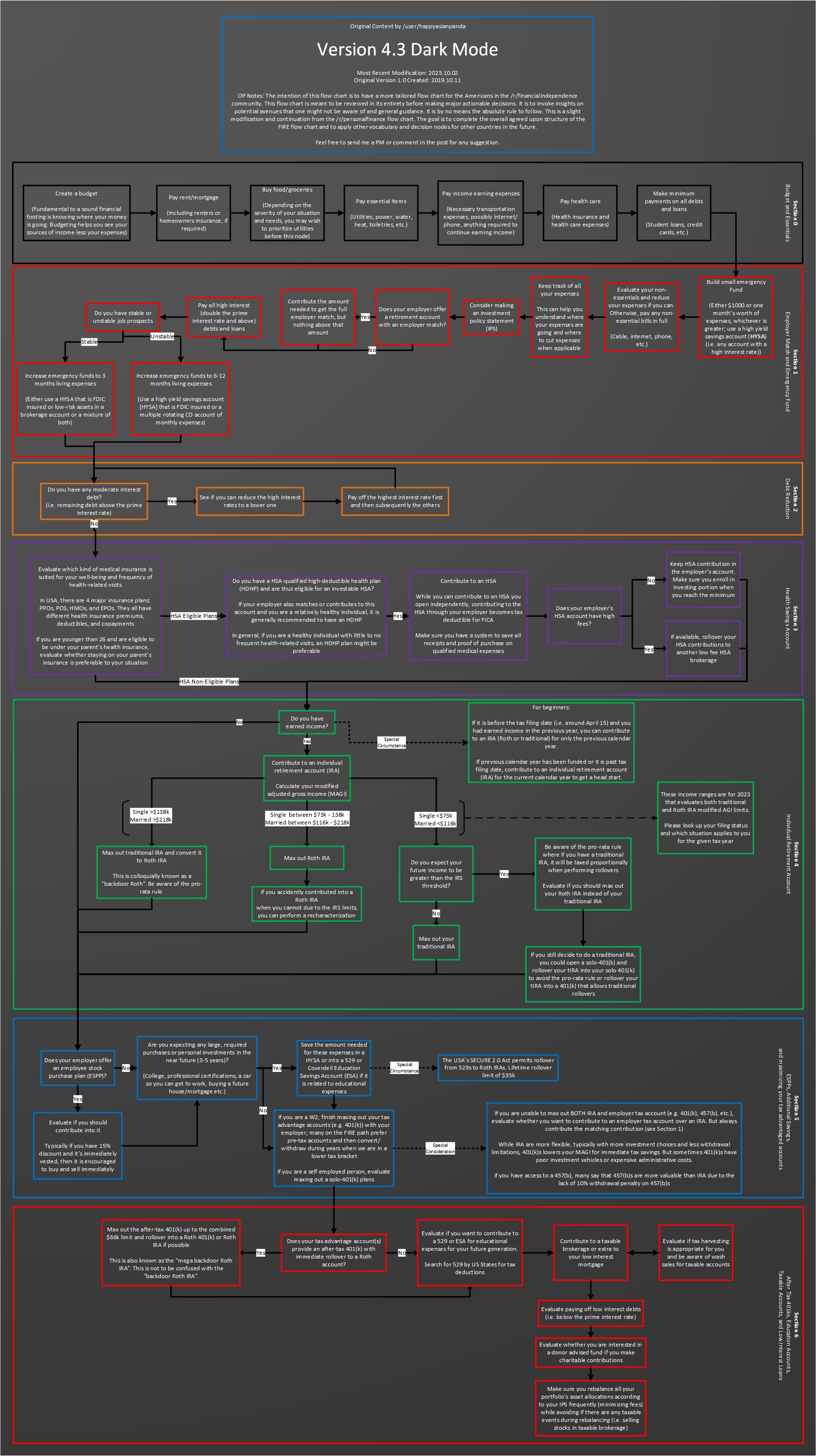

Great advice. We're fortunate enough to have completed the FIRE flowchart and are at the maximize stage of our journey.

{kind=link}

This is good advice.

If you don't have a goal in mind for your money right now, just save and invest it while putting it out of your mind.

"Some people need a budget to save; others need a budget to spend."

My suggestion would be pick a % of your income to allocate as "fun money." 5%, 10%, whatever; the most important part is you budget it. Stick it in its own savings account, then invest the rest. Then, whenever you have the opportunity to do fun things, spend extra on hobbies, help family, donate, etc, you know exactly how much you can spend.

This is good advice. You want to save this for a better retirement, but not to the point where you can't have fun in your life.

My father used to spend his bonuses on family trips. Back when we were kids, we had so many great memories with our parents. Father always made sure to take as many photos as possible.

Looking at those photos, makes me I want to do the same for my kids as I loved it to bits, but a bit difficult nowadays with everything being way too expensive.

However, I learned that trips, adventures, hikes, or any family activity builds trust, memories, relationship, and an opportunity to capture a lot of great photos for the future.

24k a year, I would put 7.5 in my ROTH IRA, 10 in emergency fund, 2.5 for kids college. If emergency fund is ready I’d give kids more.

Budget 1500 of it to investments and savings. 300 of it to charities of your choice ideally locally focused ones like food banks, shelters, housing programs, etc. Use the last 200 as hobby or fun money to take your family out to a couple extra events or eating out.

hard to argue with that. honestly i may just follow that advice myself

Yeah. 75/15/5 is a rule I use for my own budget for all the money left over after my standard bills are paid. As long as the majority goes to accounts that earn good interest (CD's or index fund investments) it'll be fine.

If you have extra money, you can invest that to become more money. That's probably the most mature thing to do. Otherwise just hookers and cocaine..

I fund hobbies, but before I do that, I make sure me, my friends, my dog, and things in the home can be taken care of.

I'd seriously consider donating some of it.

VT and chill

How old is the kiddo? Old enough to have a creative hobby? Fund that hobby.

- Maybe they like drawing. Take them on a $300 shopping spree at the art store.

- Maybe they like competitive dancing/performing. Spend the money on a trip taking them to a competition in another city/state/country.

- Maybe they like woodworking. Let them buy the tool(s) they need to take their craft to the next level.

- Maybe they like coding and computing. Send them to a kid-centric coding camp.

- Maybe they like making music. Buy them that new instrument or private instruction on how to get better with the one they have.

Whatever it is (that is a creative hobby, not just Fortnite skins), letting them move forward with it can help them grown and succeed in ways you can't imagine decades from now.

Too young to have any real interests yet. I was considering starting swim lessons, that's a lifelong skill.

Swimming lessons is really good. Should be mandatory imho. You can start at age 5-ish and you'll be done in a year or so with the essentials.

My 2 cents: Invest it in something pretty stable (to counter inflation) and if you or your family doesn't need it later (wait until your kid is financially stable) donate the money to a good cause.

Invest.

I got a great cryptocurrency to present to you!

/s